First.The global low-carbon resonance background, photovoltaic demand is highly booming.

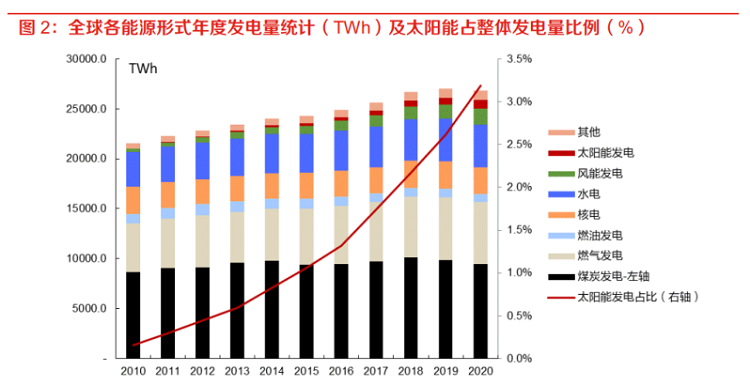

Photovoltaic industry: energy independence overlaid with low-carbon resonance, demand shows a high boom. Photovoltaic power generation costs continue to decline overlaid with the global green recovery, the PV industry as a whole is in the growth period. Global warming and resource depletion have become a common global threat, and many countries around the world have proposed "carbon neutral" climate goals. Photovoltaic power generation is being promoted as a clean power generation resource, and from 2009 to 2021, the cost of photovoltaic power generation will be reduced by 90%, making it a competitive form of power supply. With the gradual maturity of PV technology, the penetration rate of PV power generation in the world is gradually increasing, from 0.16% in 2010 to 3.19% in 2020 according to BP data. Looking ahead, PV LCOE will continue to decline and driven by the global carbon neutral background, the PV industry demand is expected to usher in firm growth, according to CPIA forecasts, by 2025 the global annual new PV installation is expected to reach 270-330GW level level.

Green and low-carbon development has become a global consensus, and the development of the photovoltaic industry has been vigorously promoted. Since the promulgation of the Renewable Energy Law in 2010, policies to promote the development of photovoltaic and other clean energy have been frequently introduced, promoting the development of the photovoltaic industry from the development path, installation planning, industry subsidies, industry support, and consumption protection.

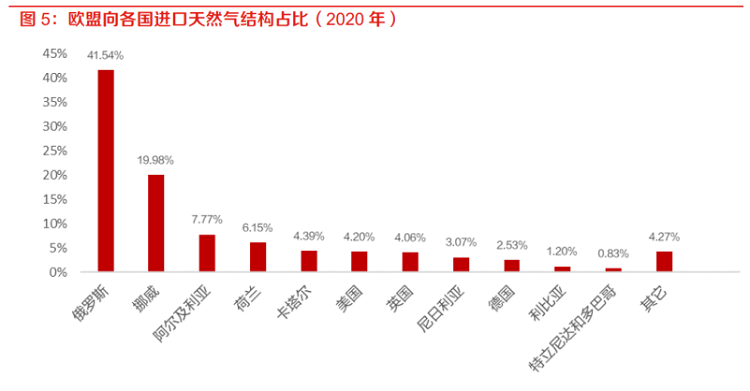

The Russian-Ukrainian conflict has brought about potential changes in energy supply, and the focus on energy sovereignty has brought new support for PV development. 2022 will affect the European energy system, making it more challenging for Europe to transform and upgrade its energy sources. Europe's energy dependence has always been high, in the overall energy pattern turbulence, accelerate the development of new energy power, become one of the effective options to enhance the independence of energy supply. In Germany, for example, the cabinet passed a package of bills (or Easter bill) on April 6, 2022, which plans to provide 80% of electricity from renewable sources by 2030 and almost all electricity from renewable sources by 2035. According to the bill, Germany's solar power capacity will increase from the current 59GW to 215GW by 2030.

Germany's renewable energy sources currently consist mainly of wind, solar and hydropower, which account for about 42% of supply. The bill says that the Russia-Ukraine conflict has brought about a turnaround in Germany's energy supply, and energy sovereignty has become a security issue for Germany and Europe. The spread of energy independence sentiment is expected to provide strong support for the subsequent growth of photovoltaics. In addition, on April 7, the U.K. also updated its energy security strategy on the government's website, with solar energy as part of the new strategy. Energy independence sentiment is spreading, bringing new support for PV development.

Second. The global new PV installation continues to grow, distributed PV is expected to continue to increase the proportion of.

The proportion of distributed PV installations is expected to continue to grow, with the rapid development of centralized PV in developing countries and regions such as China before 2016, which is faster than distributed PV, making distributed PV account for a decline in the proportion of new PV installations worldwide, from 43% in 2013 to 26% in 2016 against the background of increased new installations. Since 2017, the proportion of global distributed PV new installations has rebounded significantly relative to the previous, mainly due to:

First, Europe, the United States, Australia and South America and other countries and regions to enhance environmental awareness and clean energy awareness, abundant light resources; second, in many of the aforementioned countries and regions, photovoltaic power generation has gradually become cost advantageous; third, the role of government policy support to promote. According to IEA forecast data, 2022 distributed share of short-term decline, we believe that is mainly due to 2021 PV module prices are at a high level, inhibiting the implementation of more price-sensitive centralized projects, so 2022 with module prices are expected to gradually fall from a high level, centralized short-term suppressed demand will usher in a phase of recovery growth. In the future, based on the advantages of distributed PV power generation in terms of power generation, grid connection, conversion and use, and avoiding power loss caused by long-distance transmission, the proportion of new installations of distributed PV worldwide is expected to continue to increase.

|

6 Keji west road. Hi-Tech Zone Shantou City, GuangDong,China

6 Keji west road. Hi-Tech Zone Shantou City, GuangDong,China +86-0754-81888658

+86-0754-81888658 multifit@multifitele.com

multifit@multifitele.com